")

Hello. I am hoping someone can advise or give some direction on how to handle this situation in IFS.

- Parent company received an order. Billing for the order will be done by parent and depends on milestones achieved. Parent sets up the customer order.

- Most of the work will be done by subsidiary.

- Part of the revenue will be earned by parent. The rest of the revenue will be earned by the subsidiary.

- Subsidiary sets up an intercompany order (customer is parent) and project.

- The amount of revenue to be recognized by parent each month depends on the percentage of completion of the project in the subsidiary.

- Parent will not recognize cost.

- Subsidiary recognizes revenue each month based on percentage of completion. Cost recognized is actual cost.

- After subsidiary completes project, it ships to the customer. It will then bill the parent.

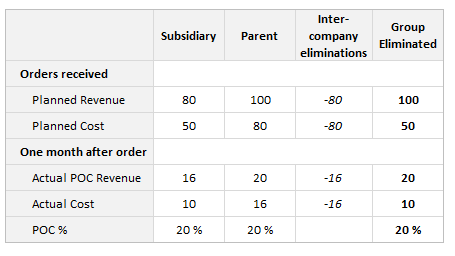

For example,

- Assume the parent received a $100 order.

- Parent sets up customer order for $100.

- Revenue allocated to parent is $20. Revenue allocated to subsidiary is $80.

- Subsidiary’s planned cost is $50.

- Subsidiary sets up an intercompany customer order and also sets up a project.

- In month 1, subsidiary’s cost is $10, so percentage of completion is 10/50 = 20%. Therefore, revenue recognized is 20% * 80 = $16.

- In month 1, parent recognizes revenue of 20% * 20 = $4 . No cost is recognized.

- In subsequent months, the subsidiary recognizes actual cost and revenue based on percentage of completion. The parent recognizes zero cost and revenue based on the subsidiary’s percentage of completion

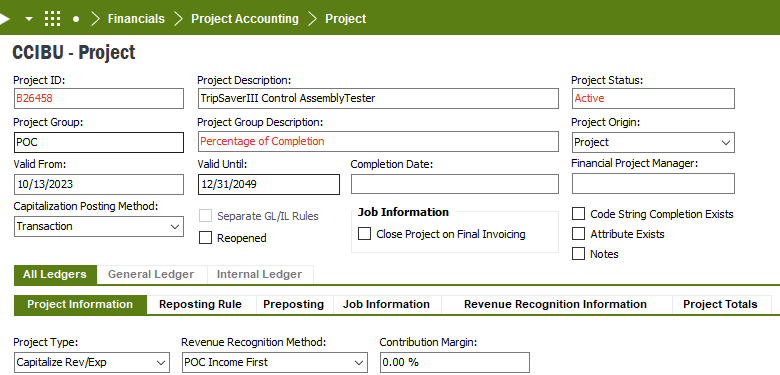

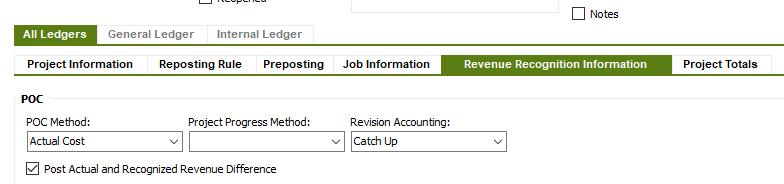

Our subsidiary normally sets up an order and project. A financial project is also set up with project type Capitalize Rev/Exp and POC Income first. So whatever the subsidiary needs to do it does correctly. Out problem is the parent’s side of the above situation. There is an order and no project. Yet we would like revenue to be recognized somehow based on the percentage of completion of the subsidiary project. Is this at all possible, or is there some other setup that would mimic this? At the moment we are recognizing the parent’s revenue via journal entries, which is not ideal. We are on Apps 9 Update 13.

I would appreciate any thoughts and ideas.

Best answer by andrei.borromeo

View original")

")

")